Home

Home

Artists

Artists

Search

Search

Recent

Recent

Random

Random

Posts

Posts

DMs

DMs

Tags

Tags

Random

Random

Importer

Importer

Import

Import

FAQ

FAQ

Account

Account

Register

Register

Favorites

Favorites

Login

Login

SIVR Silver Paper Trade. For Learning Purposes only (Patreon)

Published:

2021-02-02 16:15:21

Imported:

2022-03

Content

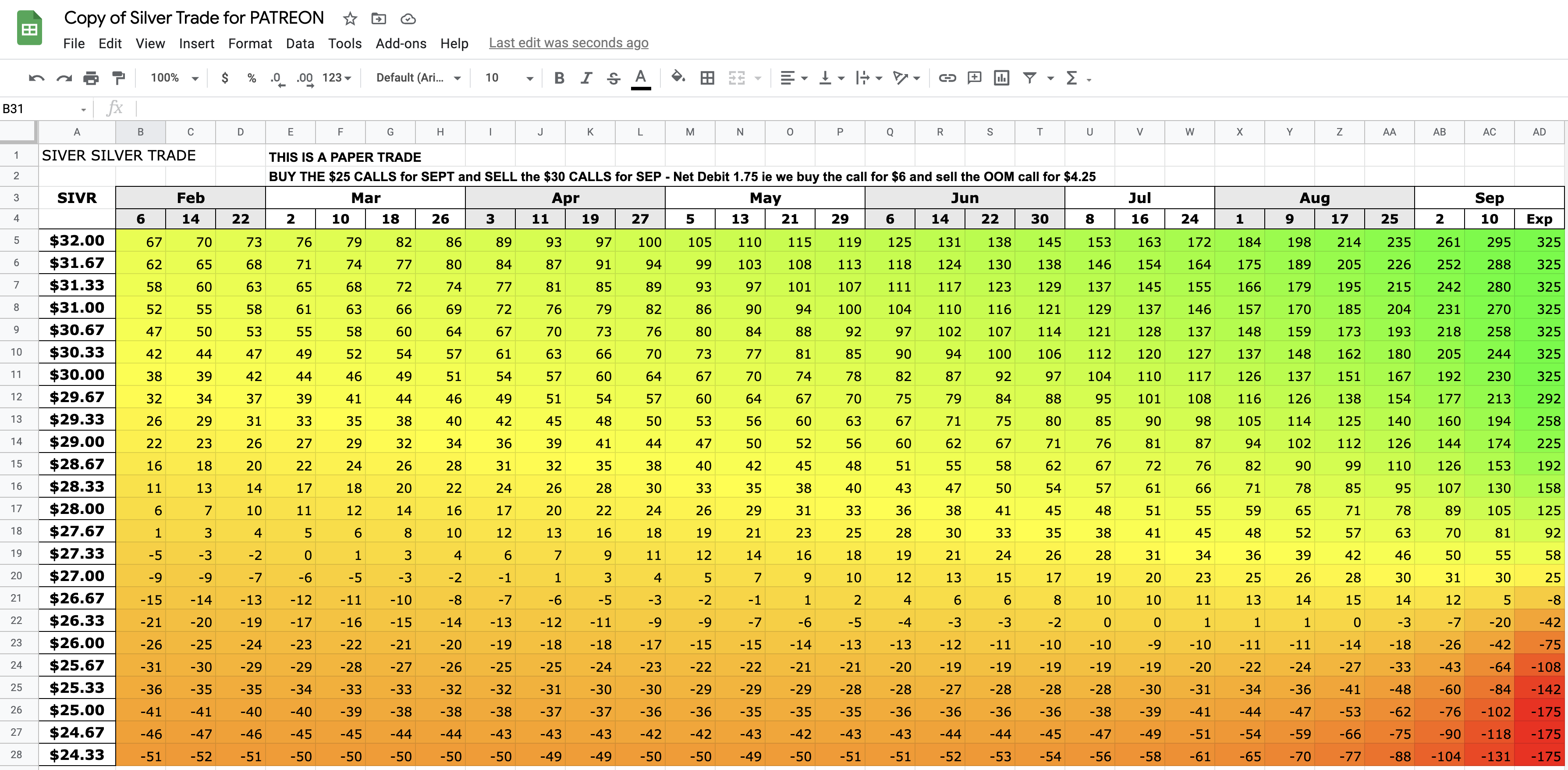

Hey everybody I want you all to get familiar with this because this gives you an idea of some option basics. It shows the effect on the combination of price of buying a call and selling it out of the money calls and the impact of time depleting the time value of the out of the money calls and also highlighting how breakeven points vary overtime by strike price. I just want you to all start thinking in these terms.

This is from my PAPER (Theoretical Trade I did not make) from yesterdays video. Google Sheet is here https://docs.google.com/spreadsheets/d/1qLdEx6NVxJnLxcePdNCCpXzJIuCcd8HyvJ07tC2P4sg/edit?usp=sharing

Files